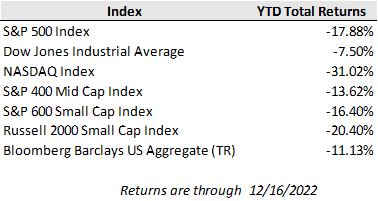

Despite last week’s encouraging CPI release showing further moderation in consumer price growth, U.S. equity markets logged a second consecutive week of losses as recession concerns grew in response to the Federal Reserve maintaining aggressive monetary policy pressure amid signs of weakening growth. For the week, the S&P 500 fell 2.1%, while the Dow Jones and Nasdaq Composite lost 1.7% and 2.7%, respectively. Bond markets rallied higher as interest rates edged lower on falling growth and inflation expectations. The U.S. 10-year Treasury yield ended the week just below 3.5% after having touched as high as 4.25% in October.

As expected, the Federal Reserve raised short-term rates by 0.50% last week—which was a step down from the recent 0.75% hike cadence—bringing the Fed funds target range to 4.25% to 4.50%. However, central bank members also continued to revise their future inflation expectations higher and increase their interest rate forecast for the coming years to rein in those price pressures.

The Fed now expects that core inflation will end 2023 at an annual growth rate of 3.5% and that the Fed funds rate will close the year at 5.1%, based on the median dot plot projection released last week. This projection is at odds with the bond market, which has priced in a more optimistic inflation outlook with price growth slowing to close to the Fed’s 2% target by the end of next year. Fed Fund futures point to the Federal Reserve raising rates up toward 5% by next spring before cutting rates down to 4.25% in the second half of 2023. The disconnect reflects the market’s expectation that a swift deceleration in growth and inflation will encourage equally swift rate cuts, whereas the Fed has communicated plans to hold rates higher for longer to ensure that price stability is indeed restored and to prevent reigniting inflation from easing policy too soon.

Measures of U.S. economic growth, while resilient to this point, are looking more strained under the growing policy pressure. Last week’s releases of retail sales and industrial production showed both measures contracted more than expected in November. Monthly retail sales fell by 0.6% against the consensus forecast for a 0.1% decline as some holiday spending was pulled forward to October and consumption continues to shift away from goods toward services. The decline in industrial production, which fell 0.2% in November against expectations for 0.1% growth, also reflects the waning goods demand. Neither of these reports point to a collapse in spending but economic growth expectations did take a step lower in response.

The week ahead will be a relatively quiet one as we close in on the holidays and year end. Several large U.S. companies (including FedEx, Nike, and Micron) are on the docket to report earnings results, but the largest focus will be on a slew of housing data reports alongside the November report of personal income, savings, & consumption expenditures. The swift decline in housing data is expected to continue (the pending home sales index was down 37% year-over-year in October and U.S. home prices broadly have been trending down since June), which should gradually feed into cooling inflation readings next year.

From everyone at First Merchants Private Wealth Advisors, we wish all of our readers a happy holiday season and a prosperous New Year.