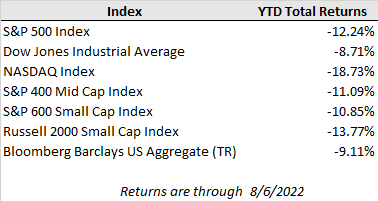

Despite the growing fears of potential recession after two consecutive quarters of falling U.S. economic output, the July jobs report soared past expectations and showed continued robust hiring that runs counter to the narrative of economic weakness. However, for financial markets the good news of a robust employment picture was interpreted as bad news in terms of future rate hike expectations as it further reinforces a more aggressive tightening stance from the Federal Reserve to rein in overheating economic conditions and inflation. U.S. equity markets still managed to cap off a third straight week of gains though, with the S&P 500 eking out a gain of 0.4%, while the Nasdaq Composite rose 2.2% and the Dow Jones ended down 0.1% on the week.

Meanwhile, interest rates pushed higher with the strong jobs report, but short-term rates are rising much more aggressively than long-term rates causing the yield curve to invert even further. The 2-year Treasury now yields 0.45% more than the 10-year Treasury, compared to a 0.26% difference at the end of July. The deepening inversion is consistent with expectations that the central bank will need to press on the brakes harder in the short-term with more rate hikes before eventually cutting them back down once inflation has come down meaningfully. Markets now point to a Fed Funds target rate of 3.50% to 3.75% by year end or another 1.25% of rate increases, according to FactSet.

The July employment release recorded a payroll increase of 528k, a pick-up from the prior 3-month average of 384k net new jobs and well beyond the consensus forecast for just 250k additional payrolls. The unemployment rate fell to just 3.5% and hourly earnings growth remained steady at 5.2% year-over-year. Most of the upside was driven by the service sector, which posted an impressive 402k increase in jobs in July as consumers continue to shift spending from goods to services.

While the jobs report was an important data point, this week’s release of July inflation readings is likely to garner even more attention. The recent decrease in commodity prices is expected to drive some moderation in price growth. July’s consumer price index reading, due out Wednesday, is expected to show a headline increase of 8.7% year-over-year (or 6.1% excluding food and energy costs), compared to a 9.1% annual increase in June (5.9% ex-food & energy).

This weekend, the U.S. Senate narrowly passed the Inflation Reduction Act, which aims to cut government deficits and dampen medical and energy costs while boosting climate spending. The bill is projected to come with a price tag of $430B, though would also aim to increase tax revenue by $739B, thereby reducing the budget deficit by roughly $300B over a decade. Market response to the news has been muted as the fiscal impact of the bill is expected to be limited over the next few years with new spending offset by higher corporate taxes. Analyst estimates of the impact of the proposed 15% alternative minimum tax on corporate income and 1% excise tax on stock buybacks are for a headwind of roughly 1-2% on 2023 S&P 500 earnings per share.

In the week ahead, while inflation updates will be the market focus, corporate earnings reports will continue to trickle in as the second quarter earnings season wraps up. With 90% of the S&P 500 quarterly results in the book, corporate earnings have remained stronger than feared as the index is on track for a 6.7% year-over-year increase in earnings for the quarter compared to expectations for just 4.0% growth at quarter end. However, one third of the consumer discretionary sector has yet to report, which could lead to some volatility in the final result given strong shifts in consumer spending.