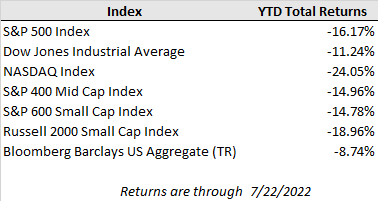

U.S. equities posted their largest weekly gains in a month last week as beaten down growth stocks surged while long-term interest rates dipped lower. Corporate earnings results, while somewhat underwhelming, have generally come in better than feared so far, lending to optimism of continued resilience despite a difficult economic backdrop. For the week, the S&P 500 gained 2.5% and broke back above its 50-day moving average, while the Dow Jones rose 2.0% and the tech-heavy Nasdaq Composite surged 3.3%. Meanwhile, the 10-year Treasury yield continued to slide lower closing the week at 2.79% compared to 2.93% in the week prior and below the 2-year Treasury yield of 2.99%. Falling long-term rates and the inversion compared to shorter maturities reflect growing market expectations for the Fed to hit the brakes on economic growth with sharp short-term rate hikes before eventually cutting rates back down once inflation shows signs of meaningfully decelerating.

With a quarter of the S&P 500 constituents having reported second quarter earnings results to date, investors are starting to get a picture of how well companies are sustaining growth in the face of headwinds like inflation, supply disruption, geopolitical conflict, and tightening financial conditions. According to FactSet, the index is on track for a 10.9% increase in revenue and a 5.0% increase in earnings for the second quarter compared to the high bar set a year ago. In aggregate, companies are beating expectations by 3.6%, though this is below the 5-year average of 8.8%.

Parsing through the individual company results, the read through so far on the health of consumer spending—the most important driver of U.S. economic growth—has been somewhat of a mixed bag but continues to point towards a strong shift from spending on items like durable goods towards services. Last week American Express, which is leveraged to spending on travel, hospitality, and entertainment, reported a 31% surge in revenue year-over-year for the second quarter.

Meanwhile, results from large bellwethers like AT&T and Walmart have painted a less rosy picture. Walmart has cut its fiscal year earnings guidance by 10% because of notable margin pressure from inflation. The retailer reported that higher food and fuel prices are denting discretionary spending and requiring markdowns on apparel and other inventory. AT&T reported a large drop in quarterly cash flow, citing the impact of customers taking longer to pay their monthly phone and internet bills. These results indicate growing pressure among lower income consumers in particular to cut back on discretionary spending in the face of rising food and energy costs.

The week ahead is chock-full of potentially market moving events. Big tech earnings are on deck in the most important week of the corporate earnings season in which over a third of the S&P 500 index members will report results. Meanwhile, the economic calendar is also packed with updates on new home sales, consumer confidence and spending, durable goods, and the first look at second quarter GDP, which is expected to contract for a second straight quarter. But perhaps the most anticipated event this week is the Federal Reserve meeting ending on Wednesday. The central bank is widely expected to raise rates by 0.75%, bringing the federal funds rate to 2.25%-2.50%, which is generally considered as “neutral” territory by the committee (neither being accommodative or overly restrictive). The bigger question from the meeting will be how the central bank sets up expectations for the next meeting in September with the market split between expectations for a 0.50% hike and a 0.75% hike while inflation continues running hot.