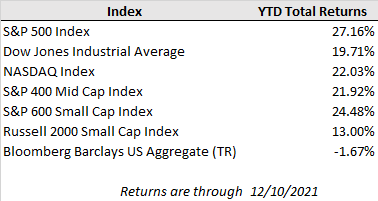

Despite another lofty monthly inflation report, U.S. equity markets rebounded sharply higher last week as market sentiment improved with early data continuing to point to mild symptoms for the Omicron Covid-variant. Vaccine news also tilted positive with an update from Pfizer and BioNTech that three doses of their Covid vaccine provides good protection against the variant, particularly when it comes to severe illness. For the week, the S&P 500 surged 3.8% to close at a new all-time high while the Dow Jones and Nasdaq Composite posted gains of 4.0% and 3.6%, respectively. Meanwhile, strong economic data and easing Covid fears also pushed long-term interest rates higher with the 10-year Treasury yield ending the week at 1.49%.

The November CPI release marked the highest year-over-year increase in consumer prices in nearly 40 years with a 6.8% headline increase compared to a year ago. Core CPI (excluding food and energy) rose 4.9% year-over-year. Automakers, who have been seen as a bellwether for global supply chains, have been noting that the worst of the chip shortage is past us, but auto production hasn’t yet brought new and used car prices under control. New and used car prices rose 1.1% and 2.5% in November and are up 11.1% and 31.4%, respectively, over the past year.

While rising prices have put a dent in consumer sentiment in recent months, improving wage and employment prospects have helped provide an offset. In fact, the December consumer sentiment survey from the University of Michigan showed consumption expectations rebounding higher driven by the largest monthly gain in sentiment since 1980 for households with incomes in the lowest third of the income distribution. The catalyst for renewed optimism among lower income households was a building expectation for wage increases in the year ahead as the job market remains tight.

For financial markets, the important takeaway from another elevated inflation reading and a tight labor market is that it reinforces the expectation that the Federal Reserve will need to act faster to reduce accommodative monetary policy in order to rein in inflation. The Fed will meet this week and is expected to announce an acceleration in the tapering of monthly bond purchases with some analysts expecting central bank bond purchases to be done by the end of March of next year rather than June, as was initially indicated. A faster taper would give the Fed more flexibility to consider tightening financial conditions by hiking short-term interest rates. The market has priced in an increase of roughly 0.68% in U.S. short-term rates (implying 2 to 3 rate hikes) in 2022 compared to a 0.29% increase at the end of the third quarter, according to the CME FedWatch Tool.

In the week ahead, while the Fed’s December meeting will garner the most attention, several important economic data releases are also on the docket including monthly retail sales, housing starts, and industrial production. Additionally, market participants will be watching trading activity as we close in on year-end following 11 straight weeks of net inflows to equity markets that have brought U.S. equity market inflows to over $365B in 2021, according to Bank of America’s Flow Show report.