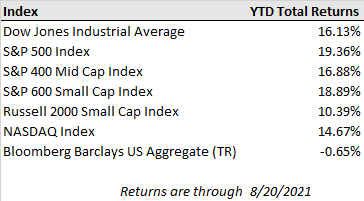

U.S. equities broadly slid lower last week amid a turbulent stretch of news headlines highlighting moderating global economic growth data, challenges posed by rising infections from the Covid-19 Delta variant, and mounting geopolitical tensions with the U.S. military pull-out from Afghanistan. Despite the headline volatility, continued inflows to equity markets provided support and erased some of the week’s earlier losses. For the week, the S&P 500 ended just 0.6% lower while the Dow Jones and Nasdaq Composite posted losses of -1.1% and -0.7%. Most of the selling pressure was within cyclical sectors like energy, financial services, and materials, while more defensive sectors like healthcare and utilities provided positive returns. Smaller capitalization companies, which tend to be more leveraged to the economic growth outlook, also tumbled lower with the Russell 2000 index posting a -2.5% loss. However, small caps and cyclical stocks have regained some ground in early trading this week with the official full approval of the Pfizer and BioNTech Covid vaccine by the FDA.

In addition to robust corporate earnings growth, the large amount of excess liquidity and cash on the sideline continues to serve as a significant source of support for equity markets, particularly as real interest rates remain so low and alternatives to equities look less attractive. According to Bank of America’s Flow Show report, U.S. equities brought in $12.8 billion in inflows in the week ended August 18, which was the largest inflow in nine weeks as investors sought to take advantage of the dip early last week. Corporate cash piles remain elevated as well and may serve as another source of demand for U.S. equities as companies buy back stock. There were $680 billion of open buyback program authorizations for U.S. companies as of the end of July, the second highest mark since 2000, according to FactSet.

While equity markets in the U.S. and other developed nations have generally continued to grind higher this year on the back of the vaccine rollout and stimulus support, emerging market equities have stumbled over the past several months due to slowing growth, lower vaccination rates and the impact of the Delta variant, as well as regulatory concerns in China, which carries the greatest weight among emerging market indices. In recent weeks, Chinese authorities have increased anti-monopoly regulations targeting large internet stocks and have started to broaden their corporate scrutiny and tighten rules in other industries including education, healthcare, liquor, and the gig economy. The uncertainty regarding the extent of the crackdown alongside slowing economic growth data and rising coronavirus restrictions have pushed Hong Kong’s flagship Hang Seng Index down by about 20% off of its high posted back in February, as of Friday’s close.

In the week ahead, market participants will be watching U.S. vaccination trends for any changes following the official approval by the FDA. Additionally, there is a full slate of economic reports including new and existing home sales in July as well as an update on the U.S. consumer with July’s personal income and consumption growth on the docket. The Congressional debate on infrastructure spending will also be in focus this week as House Democrats look to push forward with the $1 trillion Senate-passed bipartisan infrastructure proposal as well as a $3.5 trillion stimulus package of healthcare, education, and climate policies, though the latter package lacks GOP backing and may take months to pass through the House before heading to the Senate where key moderate senators have expressed reticence with its size.