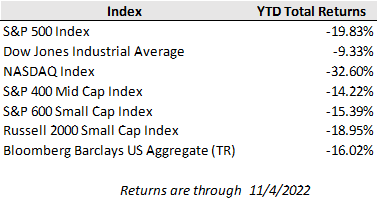

After a sharp rally in equity markets in October, November started off on more rocky footing last week as the Federal Reserve hiked rates by 0.75% and made it clear that the central bank will not be pivoting from its hawkish stance near-term. Federal Reserve Chair Powell set the tone when he warned that the ultimate level of interest rates will be higher than expected, and markets responded by pushing up peak short-term interest rate expectations above 5% for next year. For the week, the major equity indices were all lower, with the Dow down 1.4%, the S&P off 3.4% and the Nasdaq dropping 5.7%. The 10-year Treasury yield ended the week at 4.18% and the 2-year yield pushed to 4.67%, compared to 4.02% and 4.42%, respectively, in the week prior.

The robust October jobs report released Friday further strengthens the Fed’s case that financial conditions will need to be tightened further to rein in overheating economic conditions that are stoking inflation. Nonfarm payrolls increased by 261k in October, beating expectations of a 193k increase, and September’s job gains were revised higher than originally announced by 52k bringing the prior month increase to 315k. The unemployment rate ticked higher to 3.7% from 3.5%, but that was primarily driven by lower labor market participation. In all, job gains are slowing but the labor market remains too tight and is underpinning wage inflation as wage growth again surprised to the upside in October with a 0.4% increase over September (a 4.7% year-over-year increase).

As earnings season starts to wind down, third quarter results have generally disappointed with only 70% of S&P 500 Index companies posting better-than-expected earnings compared to 85% a year ago and 24% missing EPS estimates vs. 13% a year ago. Of the 409 S&P 500 companies that have held analyst calls this quarter, the word “Recession” came up 165 times. A year ago, “Recession” was uttered on 42 earnings calls by S&P firms in the entire third quarter. Profits are up just over 2% on average for S&P 500 companies that have reported this quarter, down from 6% a quarter ago, according to FactSet, which tracks corporate profits and other market data. Worse, analysts now expect that profits will decline in the fourth quarter for S&P 500 companies, which would be the first time that has happened since the start of Covid.

In the week ahead, the U.S. election on November 8 will direct some attention away from investors focused in on the Federal Reserve. The consensus expectation is that a divided government between the White House and Congress will lead to more political gridlock and a potential slowdown for some of President Biden's agenda. Historians note the stock market has outperformed with a divided government over the returns generated in the years following the same party controlling the Senate, the House, and the Presidency. Analysts warn that a scenario that could rattle the market would be any lack of clarity with regard to Senate control if results are contested. Meanwhile, the economics calendar will be dominated by the October consumer price index report released on Thursday.