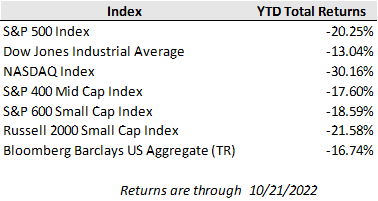

U.S. equity markets surged higher last week as market yields took a pause from their relentless year-to-date climb while investors weighed the possibility of smaller future rate increases from the Federal Reserve. The sharp impact from the breakneck pace of rate hikes has been a major contributor to this year’s selloff, so any indications of a deceleration in that pace has been met with market rallies like this past week. The major market indexes all scored their biggest weekly percentage gains since June, with the S&P 500 finishing up 4.8% for the week, the Dow Jones up 4.9%, and the Nasdaq Composite moving up 5.2%.

The latest commentary from Federal Reserve officials has pointed to growing potential for the central bank to gradually ease back on the pace of tightening. On Friday, Federal Reserve Bank of San Francisco President Mary Daly said future interest rate increases could come in smaller increments to achieve the Fed’s target neutral rate. While the Fed seems set to again move its benchmark rate up by 75 basis points at the November policy meeting, there may be some debate among Fed officials over whether to slow down aggressive rate hikes thereafter.

While easing interest rate pressures would provide reprieve to financial markets, investors are closely monitoring corporate quarterly results for clues on the extent to which the sharp increase in rates is weighing on the earnings outlook, in addition to the notable headwinds of a strengthening U.S. dollar and cost inflation. With a quarter of the S&P 500 third quarter earnings results in the book, more than 70% of S&P 500 companies have reported a positive surprise in terms of earnings per share, though quarterly earnings are on track for year-over-year growth of just 1.5%. More earnings reports will pour in the week ahead, including widely anticipated results from the tech heavyweights Apple, Amazon, and Microsoft. Meanwhile, Intel's spinoff of Mobileye Global through an IPO is also expected to generate plenty of buzz and Elon Musk's acquisition of Twitter is closing on its deadline date October 28 with plenty of drama still in the mix.

Looking overseas, stocks in Hong Kong and Shanghai closed out Monday's session down 6.4% and 2%, respectively, amid a slew of concerns over the country's economy. While third-quarter GDP growth beat expectations at 3.9%, the figure was way below China's official full-year target of 5.5%, which is already its lowest goal in three decades. A large-scale property crisis and strict zero-COVID strategy have weighed down consumer spending, and there are additional economic fears as President Xi Jinping tightens his grip on power. During China's 20th Party Congress, Xi was awarded with a third five-year term as leader of the ruling Communist Party, while the new Politburo Standing Committee was stacked with allies. Xi also reaffirmed his Common Prosperity drive by pledging to "standardize wealth accumulation mechanisms" and by promoting "Chinese-style modernization." Meanwhile, the Communist Party's constitution was amended with strengthening "fighting spirit and ability," while deterring separatists seeking independence in Taiwan.

Meanwhile in the U.K., Rishi Sunak is the next Prime Minister after Boris Johnson withdrew from consideration. His guidance for the U.K. for the next year is due to be presented next Tuesday to Parliament and the U.K. citizens.

The FOMC’s pre-meeting quiet period has begun, meaning no FOMC participant will discuss the economy or policy until after the November 2 meeting. Fed Governor Chris Waller is at a Money 20/20 Fintech conference in Las Vegas today, where he will discuss FedNow, the Fed’s new instant clearing service, expected to debut in May or June next year. Getting a Fed governor to speak at your conference is important, but Serena Williams is the biggest draw at the conference this year.