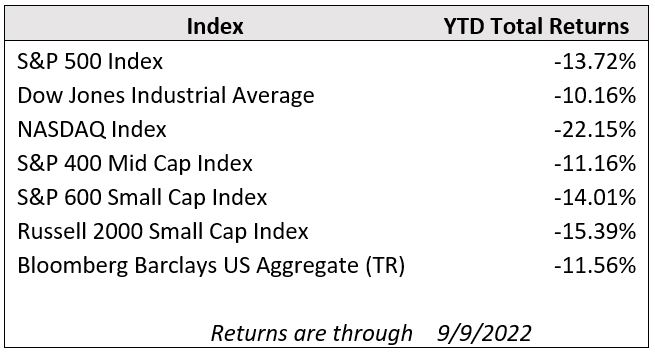

U.S. equities bounced back sharply last week after three consecutive weeks of losses with the S&P 500 gaining 3.6% on the week and all sectors in the green. However, equity markets are giving back most of those gains (the S&P 500 is down roughly 3.0% at the time of this writing) following this morning’s August CPI release that showed consumer price inflation surprising to the upside. The tug-of-war between bullish and bearish perspectives that has sent markets whipsawing over the last few weeks boils down to whether the Federal Reserve can restore price stability without crushing economic growth. This morning’s report reinforced expectations that the Fed may need to ramp up the pressure a bit more in the short-term to get the job done. The 2-year Treasury yield has climbed up toward 3.75% from 3.56% yesterday.

According to the August CPI report, headline inflation rose 0.1% month-over-month, even with falling gas prices, and core inflation rose 0.6% month-over-month. Those figures well overshot economist consensus expectations for a decline of 0.1% for overall inflation on the month, and a rise of 0.3% for core inflation. On a year-over-year basis, the rate did continue to moderate to 8.3% from 8.5% in July. Consumers got strong price relief at the pump in August with gasoline prices down 10.6%, but that improvement was offset by other key components like food and shelter, which rose 0.8% and 0.7%, respectively.

The CPI report gives the Federal Reserve the green light to continue its aggressive rate hike cadence at the upcoming FOMC meeting set for September 20-21. According to the CME FedWatch Tool, markets now price in an 82% probability of a 0.75% rate increase this month, which would bring the Fed funds target rate to 3.00% - 3.25%, and an 18% probability of a full 1.00% rate hike, which hadn’t been on the table ahead of the inflation report. In his last public appearance before the FOMC meeting, Fed President Powell said the central bank's policy interventions are aimed in part at bringing the labor market back into better balance and easing wage pressures to levels that are more consistent with 2% inflation.

Investors are also paying close attention to future corporate earnings expectations as the economic growth outlook recedes. Corporate earnings have remained resilient this year, with the S&P 500 posting an 8.7% increase in earnings per share for the first half of 2022 compared to a year earlier. However, analysts have begun to cut their future company earnings forecasts over the last two months. According to FactSet, the aggregate third quarter earnings forecast for members of the S&P 500 has fallen from 10.8% year-over-year at the end of June to 4.2% today, the largest dip in forecasts since the second quarter of 2020.

Overseas, a Ukrainian counteroffensive that began over the weekend has made substantial territorial gains in the country’s northeast pushing Russian troops out of Kharkiv, Ukraine’s second-largest city. The Ukraine army claims to have captured more than 7,000 Russian soldiers, hundreds of pieces of heavy equipment including as many as 50 tanks, and vast stores of ammunition. The Russian military has responded with precision missile strikes on power plants in several cities, but it is unclear yet whether they will mount a broader counterattack.