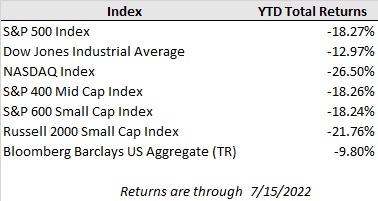

Stocks rebounded higher on Friday and snapped a five-day losing streak thanks to stronger than expected retail sales data and a moderation in inflation expectations. Financial stocks paced Friday's gains, with Citigroup surging 13% as it reported the best second-quarter results of any big bank so far. Meanwhile, comments from the president of the Atlanta Federal Reserve indicated that he likely would not support a potential 1.00% rate hike at the central bank's upcoming July policy meeting, opting instead for a 0.75% increase. But Friday's rally still was not enough to overcome three days of losses earlier in the week, leaving the three major market indexes with weekly losses of 1.6% for the Nasdaq, 0.9% for the S&P 500 and 0.2% for the Dow.

Earnings reports will dominate the week ahead as big names like Bank of America, Netflix, Tesla, and Twitter are set to report second quarter results. While investors are bracing for the potential that this earnings season will see a larger number of disappointments and downward revisions, the latest fundamental reads on consumer demand, labor shortages, and supply chain issues will still be critical to monitor.

Another key theme to keep in mind during this earnings season is the strengthening of the U.S. dollar, which is up over 12% so far this year and is now at a 20-year high against a basket of other major currencies. The constituents of the S&P 500 generate roughly 40% of their revenue in aggregate outside of the U.S., so the weakening of foreign currencies against the dollar will be a headwind to reported earnings of major multinationals.

Additionally, aggressive U.S. interest rate hikes and the sharp rise in the dollar could put the financial stability of poorer nations at risk. Paying interest to creditors in dollars has become particularly difficult for countries with rapidly depreciating currencies, such as Argentina and Turkey, especially as interest rates on any new debt will also go up. At least 75 central banks around the world have raised interest rates, many from historically low levels, and the European Central Bank is expected to make its first rate increase since 2011 at a meeting this week. Officials have signaled that a rise of only a quarter percentage point is likely, probably followed by a larger move in September.

On the U.S. policy front, the Senate could vote on a scaled-down measure to provide support to the U.S. semiconductor industry as soon as this week as lawmakers struggle to compromise on broader legislation targeting Chinese competitiveness. The bill would likely provide $52B in grants, tax credits, and other financial incentives to build out the American chip sector, but until now, it has been held up over R&D subsidies, as well as the possibility of it being attached to a broader reconciliation package. Congress will need to kick things into high gear before the August recess, which is only several weeks away.