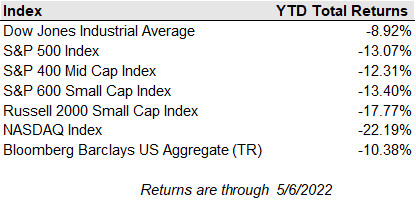

The stock market finished the first week of May with minor losses, but it was not subtle. The three major indexes started the week with three straight positive sessions, then suffered a sharp selloff after investors decided the Federal Reserve's policy tightening cycle ahead was still very hawkish, even as Chairman Powell took the potential for a 75-basis point rate hikes off the table. Investors are increasingly unsure if the Fed will be able to combat inflation without sending the United States into a recession.

Investors will be tested once again this week with the upcoming consumer price report. The consumer price report is expected to show a 0.2% month-over-month increase in CPI and decrease in the year-over-year inflation rate to 8.2% from 8.5%. Food and auto prices are seen to be still running hot, while some deceleration is seen with hotel prices, airfares, and transportation services pricing. The inflation report comes with the 10-year Treasury yield having just pushed through the 3% threshold for the first time since late in 2018.

Consumers pulled back their online spending as e-commerce transactions declined 1.8% from a year ago while in-store sales increased 10% over that period. Shopify and Etsy forecasted growth deceleration, and Amazon reported the slowest growth since 2001. Though e-commerce sales are declining, they are still significantly higher than pre-pandemic levels and here to stay. IKEA announced it will be investing $3B to add urban stores and update existing big-box locations to work as distribution hubs for online orders.

The geopolitical and economic uncertainties show no sign of abating. The Russia-Ukraine war continues, at a great human cost and with signs of escalation, while China’s COVID-19 issues persist. Attention shifts to inflation and a Federal Reserve-induced recession. The Fed no longer believes inflation is transient and has committed to bringing it closer to target. As we get further into the US earnings season, we are learning that profit margins remain healthy despite inflation. Consumer spending has been robust, new jobs are being created, and we believe growth will remain above trend despite the recent US GDP report. The US has potential to add upwards of 200,000 jobs a month until the end of 2023. The question that remains is, can the Fed engineer a soft landing where both inflation and growth move closer to trend without causing a recession?