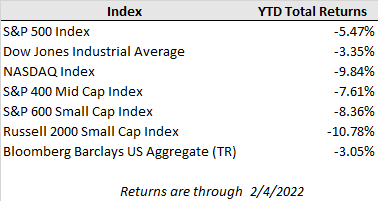

U.S. equity markets broadly posted positive returns after another turbulent week of trading driven by a mixed bag of corporate earnings results and a strong jobs report that pushed interest rates higher. For the week, the S&P 500 gained 1.6%, while the Dow Jones rose 1.1% and the Nasdaq Composite rose 2.4%. Small cap stocks, which have been hit hard to start the year and remain well below their highs from last November, also rebounded higher this past week with the Russell 2000 up 1.7%.

Extreme market reactions to earnings results over the last few weeks have left many investors feeling whiplashed. Just last week, markets saw the largest market value gain from a stock in one day on Friday with a 14% surge from Amazon that added $191 billion to the company’s market value after posting earnings well beyond analyst forecasts; however, a day earlier markets also saw the largest market value lost from a stock in one day with Meta (formerly Facebook) losing $232 billion in market value with its 26% tumble after reporting earnings and giving guidance that fell short of expectations.

While there are many factors playing into these wild market swings, much of the volatility boils down to a reset in expectations for future corporate earnings growth and the uncertainty to the future path of rates and monetary policy. To the former point, investors are trying to get a sense of how much of last year’s strong surge in corporate profits is sustainable as pandemic stimulus fades and consumer spending habits normalize. Many of the hardest hit stocks so far this year have been beneficiaries of pandemic trends where growth was pulled forward, but markets had projected out those rates of growth indefinitely as the new normal. Inflation also clouds the outlook around future earnings given the uncertainty for how long wage and input cost pressures will remain elevated and to what extent companies will be able to pass those cost increases on to consumers.

At the same time, investors are grappling with the rate at which those future corporate profits should be discounted back to today in determining present values. The Federal Reserve and other central banks around the world have shifted swiftly towards raising interest rates and reining in liquidity, but the extent to which they can and will raise rates remains an open question. Last week’s robust U.S. jobs report actually pushed long-term rates passed their pre-crisis levels as it showed economic strength that may give the Fed more room to raise rates without choking off growth. In the face of peak omicron cases, the U.S. economy added 467k payrolls in January, compared to expectations for around 150k new jobs, and the prior two months of job gains were revised upward by over 700k.

As long as markets are homing in on the natural pace of earnings growth, inflation, and interest rates, volatility will likely remain elevated. However, the fundamental economic picture remains supportive and resilient as shown by the strong labor market and robust earnings in aggregate. In fact, with just over half of the fourth quarter corporate earnings season in the books, the S&P 500 is on track for a 29% growth rate in earnings over the prior year, compared to expectations for 21% earnings growth at year end.

In the week ahead, corporate earnings and inflation will remain front and center on the minds of investors. There are 83 S&P 500 companies on the docket to report earnings throughout the week. On Thursday, the January CPI release is expected to show another step higher in the rate of consumer price growth with the year-over-year rate increasing to 7.3% from 7.0% in December. The inflation readings over the next few months will be a key determinant in the Fed’s announcement of rate hike expectations at the next meeting in March.