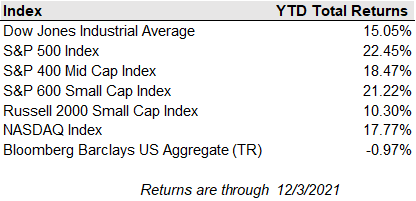

Stocks closed out the week with a drop but managed to put off some damage with last hour buying. The Nasdaq took the biggest hit of the selling again, while the S&P and Dow also finished in the red. The S&P and Nasdaq had their second-straight losing week, off 1.2% and 2.6% respectively. The Dow Industrials have been down four weeks in a row. Rates tumbled, with the 10-year Treasury yield falling 10 basis points to 1.35%. Why was everything down? They were down from comments by Fed officials suggesting that the central bank will likely double the pace of its taper at its December meeting next week despite the emergence of the omicron COVID variant. More volatility could come this month if the Fed decides to raise rates as soon as spring.

Early data on the omicron variant shows that, while it is highly transmittable, it does not have the same severity as the delta variant. A key observation from the report was that most of the patients were not oxygen-dependent, which was common in previous waves. While encouraging, it is important to note that the data sample is small, and we should still exercise caution with the omicron variant.

Nonfarm payrolls came in lower than expected for November, but the jobless rate dropped, and the labor participation rate rose. Rate expectations were moved forward and there is now a 50% chance of a quarter-point rate hike in May, according to fed funds futures.

This week could see some more risk-off trading with the consumer price index report arriving on Friday just days before Federal Reserve policy makers meet to discuss inflation risks. Analysts expect the headline CPI number to reach 6.7%, which would be the highest rate since 1982. An even higher rate could rattle investors more and change central bank expectations.