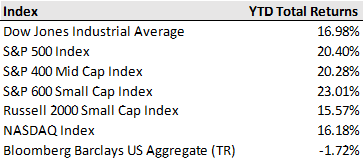

U.S. equities broadly managed to post their best weekly gains since July last week as a strong start to third quarter corporate earnings season helped lift stocks after dipping earlier in the week on concerns of mounting inflation pressures. For the week, the S&P 500 climbed 1.8%, while the Dow Jones and Nasdaq Composite added 1.6% and 2.2%. Meanwhile, commodity prices continued to surge higher with oil prices hitting multi-year highs amid energy shortages in China and Europe. Energy shortages have had knock-on effects for production of other commodities, like industrial metals, as well. Copper, aluminum, and several other industrial metals had price increases of over 10% last week alone.

The jump in energy prices bolstered the rise in last week’s September Consumer Price Index (CPI) update, which showed headline inflation remaining elevated with a 5.4% increase year-over-year. However, looking past the headline increase, the upward momentum in core CPI (excluding food and energy), which was up 4.0% year-over-year, has started to fade over the last few months. This trend will be watched closely in coming months as rising prices and the constant news of supply chain disruptions have started to erode consumer and business confidence and will play a crucial role in the path of monetary policy.

Snarled supply chains and rising input costs will also be a key theme on investors’ radars during the third quarter corporate earnings season. The season got off to a good start last week as the results of several large banks and financial service companies highlighted continued strength of consumer balance sheets and robust capital markets activity. The bar has been set high coming into this quarter with the consensus forecast for nearly 30% earnings growth for the S&P 500 in aggregate compared to a year ago, according to FactSet. However, the wide array of unforeseen disruptions over the past quarter may lead to a greater number of misses and diminishing forward guidance updates. The ability to pass on price increases may also come under pressure as consumers were likely less sensitive to price hikes when fiscal stimulus was flowing.

In the week ahead, corporate earnings will remain in focus with 355 U.S. companies set to report, including 77 from the S&P 500. The economic calendar is a lighter one this week with some updates on housing and manufacturing, though market participants will continue to track weekly employment reports closely as initial jobless claims fell below 300k last week for the first time since the onset of the pandemic.